In California, there is a controversial plan to require credit card readers on all public charging stations, including retrofitting already installed units.

California’s Electric Vehicle Charging Stations Open Access Act (Senate Bill 454, which passed in 2013) mandates open access to public charging stations – that is, a driver doesn’t have to be a member of a particular network in order to use a particular station.

However, there is disagreement about how to interpret the language of the law. The Electric Vehicle Charging Association (EVCA) – which represents several prominent companies including ChargePoint, BTCPower, EVBox, EV Connect and EVgo – and the California Air Resources Board (ARB), which regulates the law, see the requirements differently.

(This is one of a three-part report on new regulations that some argue could hold back EV charging development, originally published in Charged Issue 42 – March/April 2019.)

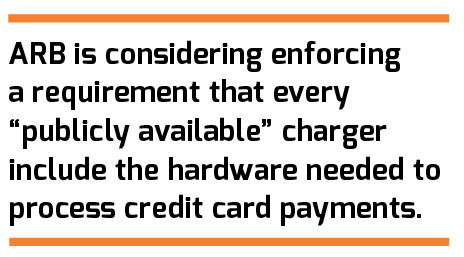

To simplify a nuanced regulatory language debate, many charging stakeholders are arguing that “open access” should include offering different payment options such as pay-by-phone or other mobile payment technologies. However, ARB is considering enforcing a requirement that every “publicly available” charger include the hardware needed to process credit card payments. Under the proposed plan, credit card readers would have to be included in all new DC fast chargers by January 1, 2020, and in new Level 2 chargers by January 1, 2023. Existing chargers would have up to five years from the date of installation to comply with the requirements.

Of course, free charging stations wouldn’t need to have card readers – the law covers only charging stations that “require payment of a fee.” However, in the rapidly evolving market for charging, the distinction between paid and free isn’t always so clear-cut. For example, some providers of workplace charging make their chargers available to the public outside of working hours. Also, station owners may want to have the option of adding or removing fees in the future, depending on how demand develops. Would any station that ever charges a fee to anyone be required to have a card reader?

Who’s going to pay for it?

This proposed requirement has inspired a lot of pushback from the industry, especially from providers of Level 2 chargers, because the additional cost of adding credit card hardware to every unit would be a greater burden than it would be for larger DC fast chargers.

Some are arguing that installing and maintaining the readers will impose substantial costs on what is already a very low-margin business (in fact, not everyone is convinced that “charging for charging” is a viable business model at all, at least for Level 2 charging). The cost of compliance with a credit card requirement could lead to the unintended consequence of reducing the availability of public chargers.

If they were forced to retrofit thousands of already-deployed Level 2 units, station owners would have to choose among three options: paying the costs to upgrade the EVSE, switching to free charging only, or deactivating certain charging stations altogether. It’s easy to imagine situations in which a site host wouldn’t see any value in reinvesting in a charging station that is not highly utilized, and would opt to remove it – particularly if the initial installation was subsidized by one of the many government grants that have been available in the past decade.

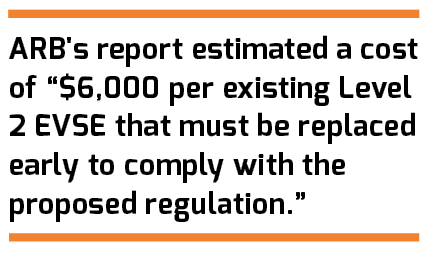

In fact, ARB released its own State Regulatory Impact Assessment (SRIA) to map out the potential costs. By its own estimate, “retrofitting payment hardware may be largely infeasible” for existing Level 2 EVSE. “As a result, many Level 2 EVSEs are projected to be replaced earlier than their natural end of useful life,” at an estimated cost of “$6,000 per existing Level 2 EVSE that must be replaced early to comply with the proposed regulation.” This cost would be borne by the site host.

Currently, many of the major networks’ public charging sites do not feature credit card readers, for a variety of reasons. One prominent exception is Electrify America, a subsidiary of Volkswagen that was established as part of the company’s diesel emissions settlement. Including credit card readers was a requirement of that settlement.

ABB is one of the largest manufacturers of DC fast chargers, which it supplies to many charging networks around the world. The company does produce units that include credit card readers, but currently finds limited demand for them. “The cost burden of transacting with credit card readers is just more complex,” ABB’s Erin Galiger told Charged. “We do offer the option, but find the most demand for it only where it’s a requirement or in the cases where a charger is not part of a network. It’s not a popular method of payment deployment.”

There is also an added level of technical complexity, because of the tough environments in which many public chargers are deployed. Charging hardware manufacturer ClipperCreek previously invested in developing a Level 2 unit with a credit card reader, but decided not to launch the product. “While engineering that product we struggled to find a supplier of card readers that could withstand all of the harsh environments that our units are designed to operate in,” ClipperCreek CEO Jason France told Charged. “In the end we decided that product wasn’t a good value for our customers and didn’t launch it. There is a lot to consider with credit card readers, including reliability, customer service, maintenance and security. It all adds to the cost.”

Future-looking options

As various new methods of payment, including smartphone apps, become more popular, credit cards are beginning to look like yesterday’s technology. Another unintended consequence of requiring card readers could be to discourage innovation in methods of paying for charging sessions. What’s the incentive to develop a new innovative payment solution that’s convenient, secure and ubiquitous, if everyone is required to cling to legacy hardware?

“We certainly don’t think that the regulations should specify a single specific technology,” agrees ClipperCreek’s Will Barrett. “Technology in the industry and the solutions that are available are evolving – we shouldn’t regulate a specific type of payment as being the only way to facilitate open access.”

One promising new payment tech is ISO 15118, aka the Plug&Charge standard, which allows a charging session to be authenticated and paid for simply by plugging in a vehicle, with no card or app required. The car communicates with the charger and the network totally behind the scenes in an easy-to-use autonomous system – you just show up and plug in. It’s foreseeable that this standard, or a new technology innovation not foreseen by a regulator, could be quickly adopted and solve roaming and access issues across the board.

It’s also worth pointing out that Tesla’s Supercharger network, which is generally considered the most advanced network in service today, does charge drivers a fee for charging, but has never found it necessary to install credit card readers. As a private network only available to Tesla owners, it would not be subject to the new requirement. However, as ClipperCreek’s Jason France points out, the requirement could prevent Tesla from ever opening up its Supercharger network to other EV drivers. “If they ever do fully open access for any electric car to use the Supercharger network, wouldn’t that be an amazingly positive thing for the industry? But if suddenly they’re governed by these other requirements, which they don’t want because there is no added value, they’ll be discouraged from doing that.”

Working together

To some, it seems that ARB is trying to solve a problem from the past that has already begun to work itself out. Five years ago, interoperability and open access among charging networks was a real issue – if a driver didn’t have a ChargePoint card (for example), they couldn’t use a ChargePoint charger. However, most of the networks have added phone numbers to their chargers, so non-members can call to initiate a charging session. And the industry is steadily innovating in the direction of interoperability. To cite just one example, Hubject, a platform that enables roaming among different charging networks, boasts over 300 B2B partners in 26 countries and is rapidly expanding in the US and China. It seems that all of the major players are already moving in the right direction for ultimate customer value and benefit.

All the representatives from ABB, ClipperCreek and other companies that Charged spoke to were quick to note that they do not want to slam the efforts and ultimate goals of ARB and other regulatory agencies. Open access and network interoperability are very important objectives to work towards, and are integral to the success of EVs. However the optimal solution for consumers that encourages continued growth is still unknown, or at least highly debated.

While the California regulators want to ensure that public charging networks are open to all EV drivers with minimum inconvenience, incorporating input from industry stakeholders is an important part of the process of developing these regulations.

Unfortunately, some worry that ARB may be preparing to move forward with the credit card requirement despite pleas from EVCA and others. In a worst-case scenario, if the two sides can’t resolve their differences, EVCA argues that charging service providers (EVSPs) will be in a bind. Where it’s not practical to simply add a credit card reader to an existing charger, providers will probably have to rip out existing stations and replace them with new, redesigned models. This must be done within 5 years of installation, or by January 1, 2023, whichever is later – far less than the projected 10-year life of a typical charging station. And there are significant fines for non-compliance: $600 to $1,000 depending on the type of violation, recurring every 45-day period up to a maximum of $37,500 until the cited violation is corrected. These fines are levied against the EVSP.

As the EVCA pointed out in a letter to ARB, faced with the expense of retrofitting chargers, “many site hosts may no longer allow the public to access the station for any period of time, or may shut down the station entirely to avoid the costs of complying with this requirement. This is especially true for charging stations that are less than profitable for owners and operators, but are nonetheless important to have in the field for consumer access.”

Obviously, this is an outcome that no one wants to see, and the irony would be enormous. California’s Executive Order B-48-18 calls for the deployment of 250,000 charging stations by 2025.

UPDATE: On April 2, 2019, ARB presented a webinar discussing “current draft regulatory language revised in response to comments received during and after the November 7, 2018 workshop.” Charged will update this report with any important details as they become available.

MORE: Several states now plan to require credit card readers on public chargers

This article appeared in Charged Issue 42 – March/April 2019 – Subscribe now.

SEE ALSO:

Determining ENERGY STAR specifications for high-power EV fast chargers proves challenging

California proposes DC metering standards for fast chargers, companies ask for more time